With over C$3 trillion in outstanding corporate debt and record ETF inflows surpassing C$21 billion in 2024, Canada’s credit markets are growing in scale and sophistication. To meet the evolving needs of market participants, the Montréal Exchange will launch a first-of-its-kind credit derivatives product, Canada Bank Credit Index Futures (BCS), on April 8, 2026*.

Based on the FTSE Canada Bank Credit Spread Index, which isolates the credit spread component of a portfolio of Canadian Bank bonds, this new contract will provide transparent, flexible and direct exposure to Canadian financial sector credit risk, enhancing your toolkit for managing credit and portfolio risk.

* The FTSE Canada Bank Credit Index Futures ("BCS") will be listed on Wednesday, April 8, 2026.

Why Trade Canada Bank Credit Index Futures?

BCS contracts are designed to complement existing fixed income tools like ETFs and total return swaps while offering distinct advantages, such as:

Targeted Credit Exposure

Gain direct exposure to the credit spread of Canadian banks through a futures contract built on a representative and liquid bond index.

Expanded Yield Curve Access

Add new liquid points to the Canadian-listed yield curve, enhancing curve construction and trading precision.

Efficient Hedging Tool

Manage spread risk, portfolio duration and liquidity needs with a standardized, exchange-traded solution.

Versatile Trading Strategies

Implement tactical credit views, replicate synthetic long/short credit positions, or execute relative value trades.

How BCS Works

Each BCS contract tracks a specific FTSE Canada Bank Credit Spread Index series tied to a basket of up to 24 Canadian bank bonds. The index is calculated using market cap-weighted credit spreads over benchmark GoC bonds and reflects a duration of ~3–3.5 years.

New Index series are published ahead of each roll period, providing complete visibility into the contract’s underlying components and ensuring price transparency throughout the lifecycle.

Contract At-a-Glance

A detailed contract specifications document is available below in the Resources section.

| Underlying | FTSE Canada Bank Credit Spread Index |

| Trading Unit |

Based on the underlying index, such that each basis point of credit spread = $50 per contract. The contract size is C$5,000 x the Contract Index |

| Price Quotation | Contract Index = 100 - Underlying Index (in %) |

| Tick Size | 1/2 Basis Points (0.005)= C$25 |

| Expiry Months | Mar, June, Sept, Dec (IMM dates) |

| Settlement | Cash-settled on the third Wednesday of the expiry month |

| Final Settlement Price | Based on the FTSE Index series on the last trading day |

| Block Thresholds |

100 contracts (1 hour reporting time) 400 contracts (reporting up to 5 p.m.) |

| CS01 | Constant at C$50 per basis point |

| Bloomberg Ticker | WCBA Index (WCBM6 Index for the June 26 contract) |

Trading Strategies

BCS is a cost-efficient way to:

- Manage credit and interest rate exposure with one instrument

- Execute synthetic credit trades without owning the underlying

- Hedge liquidity or duration mismatches

- Implement long/short and curve strategies

- Overlay portfolio exposures or express macro credit views

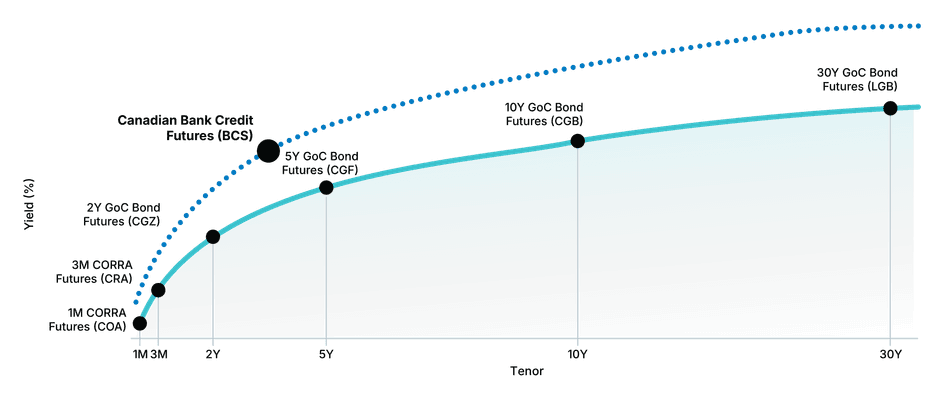

See how the BCS adds new precision points to Canada’s listed yield curve.

MX is building out the curve

What Sets the BCS Apart?

Designed with precision and transparency in mind, the BCS contract introduces key advantages that differentiate it from other credit instruments.

Index Transparency & Stability

Each contract is tied to a published Index series with fixed constituents, offering clarity from pre-roll through to settlement.

Correlation to Canadian Credit Market

The underlying index demonstrates a strong correlation to the Canadian corporate bond sector.

Simplified Construction

No need for ISDA agreements or complex structuring; gain clean exposure via an exchange-traded vehicle.

The FTSE Canada Bank Credit Index Futures ("BCS") will be listed on Wednesday, April 8, 2026.

Resources

Stay Informed

For any questions on how to access the underlying FTSE Canada Bank Credit Spread Index, please contact fi.index@ftserussell.com.

Subscribe to receive the latest updates from Montréal Exchange. Stay ahead with exclusive insights delivered directly to your inbox.

Subscribe